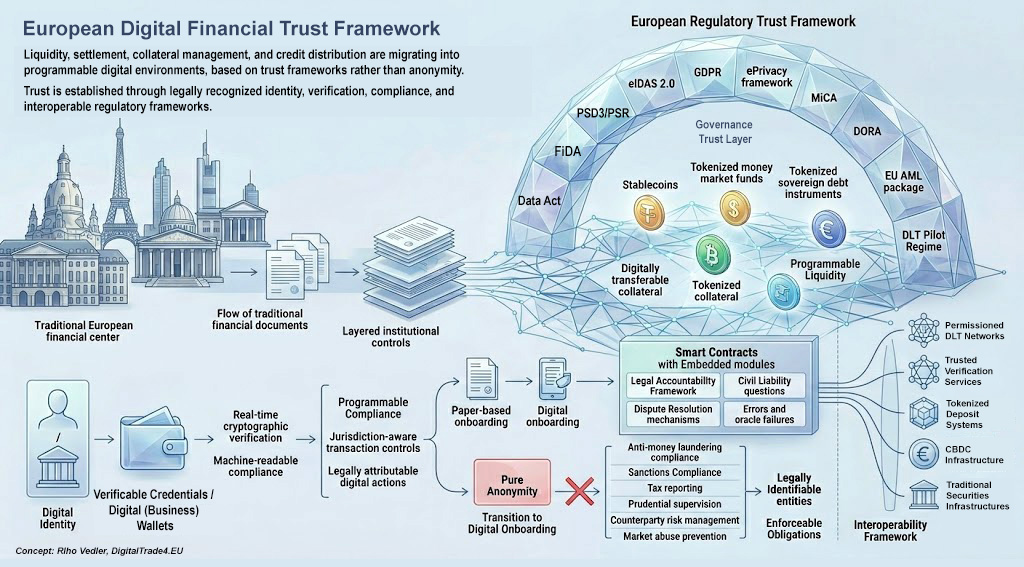

European financial markets are entering a structural transformation in which liquidity, settlement, collateral management, and credit distribution are increasingly migrating into programmable digital environments. Stablecoins, tokenized money market funds, tokenized sovereign debt instruments, and digitally transferable collateral are no longer speculative concepts confined to crypto-native ecosystems. They are emerging as components of institutional financial infrastructure.

Traditional financial markets rely on layered institutional controls involving custodians, clearing systems, settlement agents, regulated intermediaries, and supervisory authorities. Tokenized finance seeks to compress many of these functions into automated infrastructures capable of near real-time execution and dynamic collateral mobility.

The central legal challenge of tokenized finance is therefore not technological innovation itself, but whether programmable financial systems can operate within enforceable frameworks of identity, accountability, and regulatory trust.

Institutional Finance Cannot Operate on Pure Anonymity

Early decentralized finance (DeFi) ecosystems developed around pseudonymous participation models in which wallet addresses effectively substituted legal identity. Such models may function in speculative or retail-oriented environments, but they are fundamentally incompatible with institutional financial markets.

Banks, payment institutions, securities infrastructures, investment funds, and treasury operations remain subject to extensive obligations relating to:

- anti-money laundering compliance;

- sanctions enforcement;

- tax reporting;

- prudential supervision;

- counterparty risk management;

- market abuse prevention;

- and legal accountability.

Institutional markets cannot operate where counterparties are legally unidentifiable or where obligations cannot be enforced against identifiable entities.

This does not mean that future financial systems must become universally transparent. Full public disclosure of transactional relationships, treasury strategies, or commercial positions would itself create substantial legal and economic risks. Instead, institutional tokenized finance requires a framework capable of balancing privacy, accountability, and regulatory enforceability simultaneously.

Europe Is Building a Regulatory Trust Framework

Discussions surrounding tokenized finance often focus narrowly on blockchain infrastructure or digital assets themselves. In reality, institutional trust emerges from the interaction between technology, legal enforceability, regulatory oversight, and identity assurance.

The European Union is gradually constructing a broader digital trust framework through interconnected regulatory instruments including eIDAS 2.0, GDPR, the ePrivacy framework, MiCA, DORA, the EU AML package, and the DLT Pilot Regime.

Each framework addresses a different layer of institutional trust. eIDAS 2.0 establishes legally recognized digital identity and authentication mechanisms. GDPR and ePrivacy govern personal data protection and confidentiality. MiCA introduces prudential and conduct obligations for crypto-asset market participants, while DORA focuses on operational resilience and ICT risk management. The evolving AML framework strengthens supervisory and enforcement obligations across financial markets.

The DLT Pilot Regime is particularly significant because it creates the European Union’s first live regulatory environment for testing distributed ledger-based market infrastructures under controlled conditions. It allows regulated trading venues and settlement systems to experiment with tokenized financial instruments while benefiting from targeted exemptions from certain traditional financial market rules.

Individually, none of these frameworks creates institutional trust infrastructure. Collectively, however, they establish the legal foundations under which programmable financial systems may operate within the European market.

Digital Identity Does Not Replace Financial Infrastructure

It is important to distinguish between identity infrastructure and financial infrastructure.

eIDAS 2.0 does not resolve settlement finality, liquidity fragmentation, collateral mobility, or counterparty exposure. Nor does digital identity alone eliminate financial risk.

Its significance lies elsewhere. eIDAS 2.0 may provide the legal identity assurance framework necessary for trusted participation within tokenized financial systems. Through verifiable credentials, digital wallets, and legally recognized authentication mechanisms, institutions may increasingly be able to prove legal status, authorization rights, regulatory permissions, and compliance attributes through real-time cryptographic verification.

This enables real-time cryptographic verification, replacing fragmented paper-based onboarding and repetitive manual verification processes traditionally required to establish trusted compliance records.

In practice, such frameworks may support:

- permissioned liquidity pools;

- regulated tokenized collateral systems;

- programmable compliance controls;

- jurisdiction-aware transaction environments;

- and legally attributable digital actions.

However, these mechanisms only operate effectively when embedded within broader legal and supervisory infrastructures.

Smart Contracts and Legal Enforceability

The increasing automation of financial infrastructure also raises unresolved legal questions surrounding smart contract enforceability and liability.

Programmable compliance and automated execution may significantly reduce operational friction, but institutional financial markets cannot rely solely on deterministic code execution without clearly defined legal accountability frameworks.

Important legal questions remain unresolved, including:

- liability for defective smart contract execution;

- dispute resolution mechanisms;

- coding errors and oracle failures;

- reversibility of erroneous transactions;

- the interaction between automated execution and settlement finality rules;

- and the legal status of machine-executed contractual obligations.

Although DORA strengthens operational resilience obligations and ICT risk governance, it does not fully resolve civil liability questions arising from automated financial execution environments.

As tokenized financial markets evolve, legal enforceability may become just as important as technological efficiency.

Privacy and Accountability Must Coexist

One of the most significant legal challenges in tokenized finance is balancing privacy with accountability.

Institutional markets cannot function under conditions of absolute anonymity. At the same time, unrestricted transparency is equally problematic. Financial institutions cannot expose sensitive liquidity positions, funding structures, trading relationships, or treasury operations to unrestricted public visibility.

European regulatory philosophy increasingly reflects an attempt to balance these competing principles. Under the emerging European framework, it becomes possible to envision financial systems where counterparties remain identifiable to competent authorities, compliance obligations remain enforceable, and institutions can demonstrate regulatory compliance without unnecessary exposure of underlying sensitive information.

Technologically, such systems will likely rely on privacy-enhancing technologies (PETs), including Zero-Knowledge Proofs (ZKPs), which allow institutions to provide cryptographically verifiable proof of compliance or authorization without disclosing the underlying data itself.

Future institutional financial systems are therefore unlikely to operate on fully anonymous architectures, but they are equally unlikely to evolve into systems of unrestricted transactional transparency. Instead, they will depend on privacy-preserving identity and compliance models capable of reconciling regulatory oversight with legitimate confidentiality interests.

In this context, trust does not emerge from anonymity, nor from radical transparency alone. Trust emerges from legally enforceable frameworks capable of balancing privacy, accountability, and verifiable institutional participation.

Interoperability May Become the Next Systemic Challenge

Institutional tokenized finance is unlikely to develop on a single blockchain or unified technical environment.

Future financial markets will likely operate across multiple infrastructures simultaneously, including:

- permissioned institutional DLT networks;

- public blockchain environments;

- tokenized deposit systems;

- central bank digital currency infrastructures;

- traditional securities infrastructures;

- and proprietary bank-operated settlement networks.

As a result, interoperability may become one of the defining technical and legal challenges of programmable finance.

Without secure interoperability frameworks, tokenized markets risk creating fragmented liquidity pools, inconsistent compliance standards, operational silos, and increased systemic complexity. Cross-network identity verification, synchronized compliance controls, and legally reliable data exchange mechanisms may therefore become as important as tokenization itself.

The long-term success of institutional tokenized finance may ultimately depend less on individual blockchain performance and more on the ability of regulated infrastructures to interact securely and predictably across jurisdictions.

Europe’s Competitive Advantage May Ultimately Be Legal Certainty

The global competition surrounding tokenized finance is often framed as a technological race. In reality, institutional financial markets historically scale only where legal certainty and enforceability exist.

The United States has generally prioritized rapid market experimentation and innovation-led development. Europe has instead focused on constructing comprehensive legal and supervisory frameworks before large-scale deployment.

While this approach may initially appear slower, it may ultimately prove more sustainable for institutional adoption.

Large-scale financial institutions are unlikely to migrate significant liquidity, collateral, and treasury operations into infrastructures lacking:

- enforceable legal identity;

- supervisory clarity;

- auditability;

- operational resilience;

- and jurisdictionally recognized compliance frameworks.

Europe’s long-term strategic advantage may therefore lie not in speculative digital asset activity, but in building the world’s most legally trusted framework for programmable finance.

The Future of Capital Markets Will Depend on Trust Architecture

Tokenized finance is not simply transforming assets. It is transforming the legal architecture through which financial trust is established, verified, and enforced.

Future capital markets will increasingly depend on the convergence of:

- programmable liquidity;

- programmable compliance;

- digital identity assurance;

- privacy-preserving verification;

- interoperable market infrastructure;

- and legally enforceable supervisory frameworks.

Within this evolving architecture, Europe’s regulatory model may become one of the first attempts to integrate technological automation with legal accountability at institutional scale.

The future of finance will not be determined solely by blockchain efficiency or settlement speed. It will depend on whether programmable financial systems can operate within trusted legal frameworks capable of preserving both market integrity and fundamental rights.

Riho Vedler, DigitalTrade4.EU